3 warning signs that could lead to defaulting on your home loan

Defaulting on your home loan is a grim thought that no one wants to encounter. The reality is that defaulting on a home loan is a threat that is very real. Are there any signs or indicators that you may be in danger of failing victim to this?

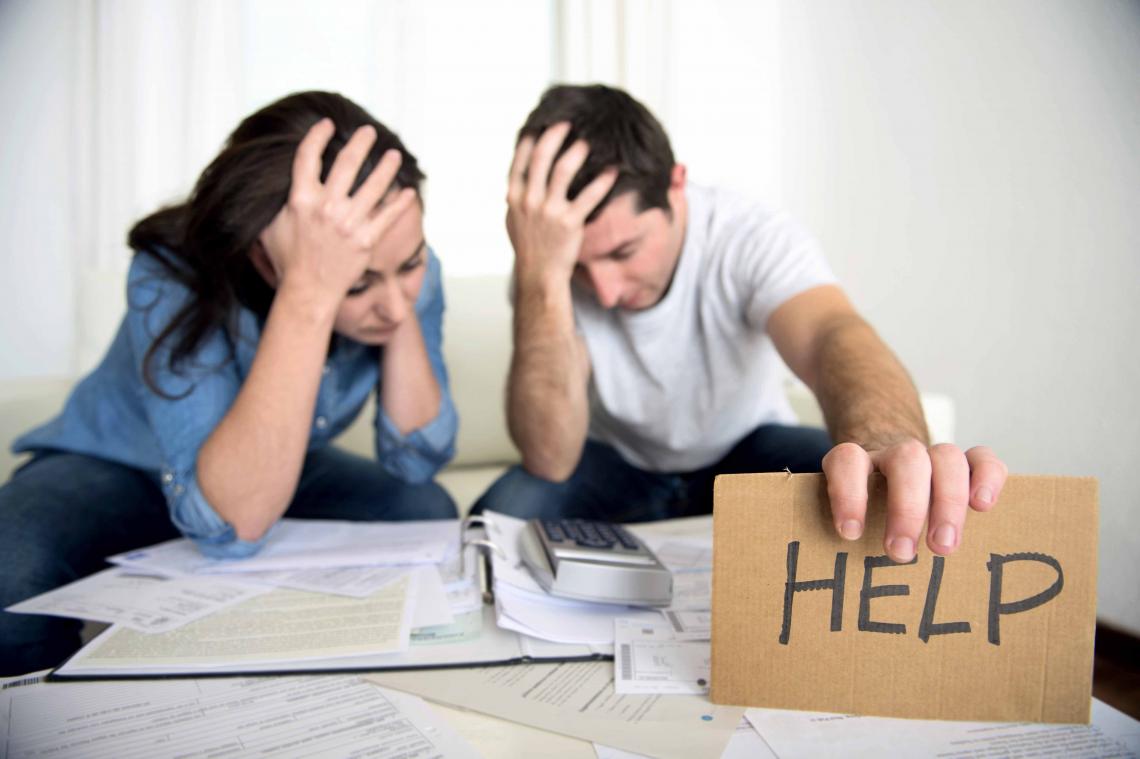

Falling on hard times financially can be a daunting and somewhat intimidating feeling. Accruing home loan debt is a scary prospect, one that is seemingly impossible to recover from. However, should the worst-case scenario occur, it's how you look to manage and recover from this that will determine your financial outcome. Knowing what indicates potential defaulting and how to deal with it is one precaution you can take.

Getting down to basics

While it may be stating the obvious, one of the biggest causes of mortgage and personal loan defaults is people not knowing or understanding what constitutes a default. A mortgage default typically occurs when a borrower is behind in making a repayment on their home loan by 90 days or more1. Before listing a default your mortgage provider must take a number of steps such as sending two separate written notices to your last known address requesting payment stating that the debt may be listed with a credit reporting body (like Equifax).

Incidents such as car accidents can potentially impact on mortgage payments.

Fees for missing mortgage payments are not exponential but are still costly. This is especially the case if you are in a negative financial situation, needing some form of personal credit repair. The primary concern lies in the interest that accrues, putting you further behind the payments on your loan.

What causes missed payments?

Missed payments are not always the result of a general financial malaise. There are often external mitigating factors such as:

- Sickness

- Loss of employment

- Sudden increase of payments (car accident, increasing insurance payments).

The above are simply some examples where a borrower's ability to make payments is affected. The important thing to do in such circumstances is to be proactive.

When a borrower is seen as having defaulted on a loan, they are sent a default notice. This affords them 30 days to make up for the payments that have got them in arrears, on top of the standard repayments that are due over that same period2.

By recognising any potential pitfalls before they happen, or soon afterward, you give yourself a chance to seek help. The important thing, according to the Financial Rights Legal Centre (FRLC) is not to panic3.

"Ring the lender and explain your situation [...] Lenders make repayment arrangements all the time. Be as clear as you can about why you are in financial hardship," says the FRLC in its mortgage stress factsheet.

Seeking the help and guidance to clarify any issues with your Equifax credit report is the first action to be taken.

Disclaimer: The information contained in this article is general in nature and does not take into account your personal objectives, financial situation or needs. Therefore, you should consider whether the information is appropriate to your circumstance before acting on it, and where appropriate, seek professional advice from a finance professional such as an adviser.

1RateCity, What happens if I default on my home loan? Accessed October 2016.

2Mortgage and Finance Help, How To Avoid Loan Default. Accessed October 2016.

3Financial Rights Legal Centre, Mortgage stress fact sheet. Accessed October 2016.

Get your Equifax credit report for FREE today

Learn moreYou might also like

How to live on a low budget while repaying your debts

Living on a low or restricted budget doesn't necessarily mean not having fun or not buying coffee anymore - it means taking stock of your financial position.

3 mistakes to avoid when you're paying off debts

Have you got debt hanging over your head? Paying it off takes time and patience - don't rush it and make one of these dire mistakes.

What are the best ways to use your credit card?

How are Australians using their credit cards? Poorly, according to research from Finder, with the average credit card balance in excess of $3,000.